🔮 Does AI make you dumb? And why our forecasts suck #576

The Sunday edition is usually reserved for paying members, but today we’re opening it to everyone. To get it every week, become a member. 🔮 Does AI make you dumb? And why our forecasts suck #576Plus, jobs in high demand, ByteDance, anti-drone nets++Hi all, This week, we published a framework to explain why individuals are getting more productive with AI, but firms often are not. Make this your weekend reading. If you want me to speak to your board about this, now is the time to book me for the fall. Linear knives in exponential gunfightsA column in the Financial Times made a fascinating observation about “the impossible maths of the AI boom.” It pointed out that in the five years to 2030…

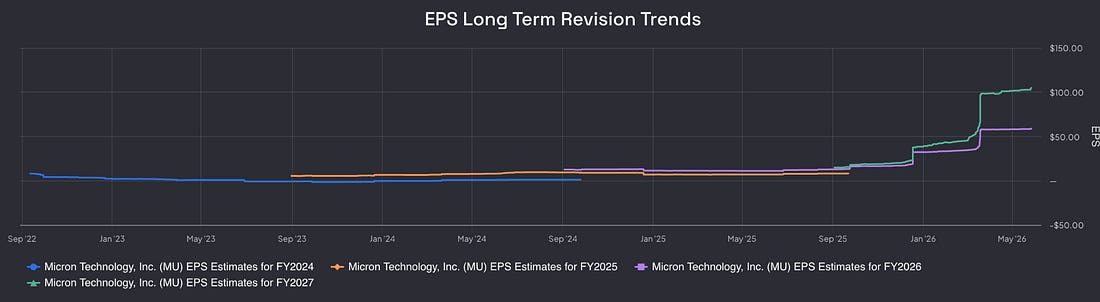

Punchy stuff. To get these conclusions about the hyperscalers' ignominious future, the author used “the consensus estimates of analysts for the capital expenditures and revenues between 2025 and 2030.” This all sounds reasonable. Equity analysts are, of course, paid very well to understand the companies in their sector and work long hours to do so. A consensus estimate is the average of what these well-heeled professionals think. The problem is that they are, on average, late to regime shifts. In particular, when a technology hits a learning curve and demand explodes, producing that familiar hockey stick, analysts often stay stuck with their old assumptions. Yes, yes, exponential curves don’t, in the real world, go on forever. But when they are going on, they are, in fact, non-linear. And the straight line and the exponential curve don’t fit well. You can see this by a simple evaluation of just how well analysts have made sense of booming AI demand. When you or I spend money with OpenAI or Anthropic, the majority of it ends up with the hyperscalers, who, in turn, are pouring hundreds of billions into buying chips, memory, and other trinkets. While Wall St analysts don’t formally track Anthropic because it is a private company, they do track those firms in the supply chain. Micron for on. Micron is an American company that makes advanced memory popular with hyperscalers. LLMs chew through memory, and Micron has done well as a result. But how well did the equity analysts covering Micron do? The chart below shows the consensus estimates for Micron’s earnings per share. Pay attention to the purple line, which is FY2026. As late as December 2025, the consensus view was that Micron would deliver about $18.25 EPS. Five months later, with some early data to help them, the median view is now about $58. So what was the point of the $18.25 forecast?

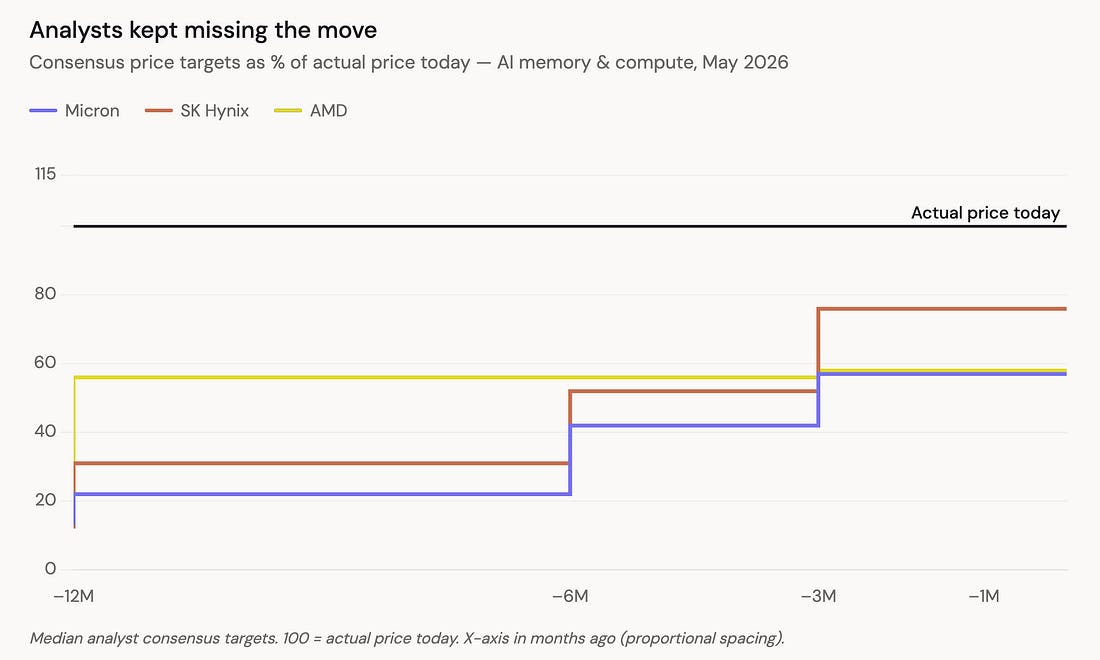

Of course, Micron isn’t a hyperscaler. But it is unusually exposed to AI. Only three companies make fancy high-bandwidth memory; Micron was the minnow and the only American player. Maybe this pattern of revisions was an exception, not the rule. Maybe Micron was just … weird. So consider a larger company like Google, with a 20-year track record. AI, understandably, is only a small part of the firm’s $300 billion revenue business. If you and I are buying heaps of tokens from Google, it’s just a drop in its overall business. But even then, between May 2025 and May 2026, the median analyst view on Google grew by 40%. What to expect with your expectationsWe all know what a share price is. It’s the price right now that's tradable on a stock exchange. But it represents a view of the future: a compressed probability distribution over future outcomes for the business. If a stock price reflects the market’s view now, an analyst's target represents something specific. It is their expectations for the stock’s value. Michael Mauboussin, a bit of a guru in the world of finance, has one of the best definitions of expected value: “the weighted-average value for a distribution of possible outcomes” of a company. So when you, I, or an analyst determines a share price target, we aren’t just choosing a number. We are expressing the outcome of the probability calculation, a distribution across possible futures for that asset. The keyword is distribution. And the shape of that distribution depends on your assumptions. If you think this is a linear, business-as-usual technology, you will make one set of assumptions. You’ll be ignoring the adoption rate, cost declines, performance improvements, or the possibility of an extreme outcome. You haven’t just chosen the wrong point on the curve. You’ve chosen the wrong curve. Sorry, sir, I misjudged the speed of that iceberg. And yet you constantly revise your expectations upwards, chasing the puck rather than getting ahead of it. Below, you can see the median analyst consensus for three companies with varying exposure to the AI wave. I’ve plotted that median expected value from 12 months ago to a month ago. They keep revising higher and are still well below what the market thinks right now.

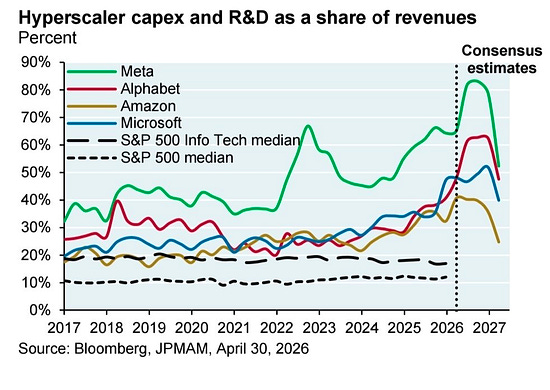

These revisions are significant. Analysts aren’t just missing the number once. They are missing it repeatedly. That isn’t bad luck; this is systematic, wilfully blind to what happens with an exponential technology. We’ve seen this before with the IEA and their two decades of comedically ignoring solar’s falling costs. Analysts covering stocks affected by the growth of AI use are doing that. Their model of the world doesn’t accommodate a range of “possible outcomes”, so the expected value (their price target) is wrong. One problem is that no-one in the major banks really covers AI in its entirety. You have chip, cloud, and software analysts. But the action, the demand action, is in private companies. A second problem is that time and again, the market is good at digesting financial information and poor at stomaching technological change. There is a sociological dimension at play, not exactly a kind of groupthink, but an intellectual tic at work. One example is reversion to the mean. Mean reversion, the idea that you can’t stay off a long-term trend for long, is a powerful heuristic. And it works most of the time, but there are some processes, especially compounding ones, where it is less helpful. Reversion is meanJPMorgan published a chart showing consensus forecasts for hyperscaler capex and R&D as a proportion of revenues. This is a data set similar to the one above, although it tells a different story, as it shows not raw dollars but share of revenue.

Assuming the hyperscalers are acting rationally, only three things could drive that slump.

Which of those three reasons can it be? On the second, it is not the job of an infrastructure analyst to forecast scientific breakthroughs, which even Demis Hassabis or Yann LeCun can’t. So it can’t be the second. Nor can it be the third — forecasting a massive exogenous tail-risk shock, a black swan that suddenly arrests the global economy, is also not their job. They are not paid to be Nostradamus. So the only possible reason is reason number one. But we’re halfway through the year; everyone is caught by growth rates, including the AI labs themselves, so what are these analysts seeing that no one else is? Nothing. The reasoning is inchoate. Truth is, exponential shifts involve regime changes, not merely rerating¹. That is uncomfortable. It is easier to assume reversion to the mean than to update your models, which worked so well in the past, with one which is dynamic, uncertain, full of feedback loops and, crucially, depends on the future being radically different to the past. That seems like hard work at best, crackpot at worst. Easier to tweak and tweak old faithful. Let’s go back to the column in the FT which questioned the rationale of AI capex investments based on consensus analyst forecasts. There is an important caveat this particular argument needs to acknowledge: it relied on consensus forecasts from a class of models that have been wrong, sometimes by an order of magnitude, on the very thing their forecasts are used for. The lesson isn’t that analysts are too pessimistic and should just revise higher. It is that consensus forecasts that are built on the intuitions of mean reversion are the wrong thing to use during regime change. It’s not about whether the numbers will surprise to the upside. It’s whether the framework can even see what’s coming. Don’t take a linear knife to an exponential gun fight. AI is making us |

|

Yes, maybe AI is making us dumber.

Here is The Economist with an interesting survey on whether AI is making us stupid. I love the irony that the site offers me an AI summary on an article that, in essence, discusses whether AI tools are making us intellectual wimps.

|

You probably recognize, feel, many of the conclusions. As we hand certain skills over to AI, those skills might atrophy. This happens in other areas, like motor skills, so it could apply to more complex cognitive activities. Some of the best things humans seem to be able to think involve integrating lots of ideas from our experiences, listening, formal instruction, doing and joining the dots.

The word intelligence is derived from the Latin intellegere. That Latinate root itself comprises inter, meaning between or among, and legere, meaning to choose, select or to read. Intelligence means “to choose between” — to connect, to join the dots.

Perhaps if we hand the actual act of intelligence (the connection-making) to AI, we’ll weaken that muscle.

If you don’t use it, you’ll lose it.

It sounds like common sense. The studies cited in The Economist provide some scientific backing for that idea.

Caution, though: these are small-scale studies. Lots of things sound like common sense until we can study them properly. That video games drive real-world violence, for example. Common sense, of course. But it doesn’t stand up to the research.

Now I don’t know if AI will destroy human thinking. My gut sense is that some things will get worse and some things might get better.

I am acutely aware of these risks. And we should take seriously what educators and students are telling us now about how their attention and quality of thinking seem to be eroding.

Thinking about thinking

Readers may imagine that with our billion tokens plus a day, Exponential View Towers is like something out of Futurama. Half of us in VR headsets, another half plugged in to our Neuralinks, and the last half deep in the Matrix.

|

But that’s not the case. Thinking is very, very important at Exponential View; we care about it a great deal. Many of our early experiments with ChatGPT focused on how it could improve the quality of those cognitive efforts, not on how we could take a shortcut through the valuable part of the process.

AI has allowed us to take away lots of “computer stuff”. Typing my essays and responding to tedious emails are now handled by RMA or Claude.² Back in December, I used to get up early to fire off new workloads. Since the models have become more reliable, I’ve been able to leave them unattended for hours at a time, whether they are running coding tasks, simulations, literature reviews or adversarial attacks on our arguments.

Paradoxically, AI has made me much more aware of my thinking processes. I have become deliberate in reflecting on my reflecting. LLMs are absolutely phenomenal and show the banality of the average. I’ve never read as critically as I do today.

Because thinking matters to us so much, we spent a lot of time figuring out how to keep mentally fit.

Here is a picture of one of our whiteboards.

|

You can see the scoping work on the thesis on why companies struggle with their AI transformations in green marker. And in the yellow box is a little exploration of Durkheim and suicide for something else we are working on. It’s more whiteboardmaxxing than tokenmaxxing.

Last year, I bought the team fountain pens. Everyone is expected to spend at least two hours a week working with pen and paper and without a computer. I don’t want to overclaim that this makes a difference; the science suggests it might.

I’m writing longhand more than I have since those halcyon days when Boris Yeltsin was a communist, Margaret Thatcher was Prime Minister and Donald Trump was married to Marla Maples. It has been a long time since I picked up a fountain pen in anger.

I’ll work on paper, while RMA will go off and do its own research. It goes through papers, my notes, and transcripts, finds what I might have missed, and counters. When I return to my screen, I am several steps further than I would’ve been without it. But I’m sceptical about its arguments. Sometimes they clear a mental block. Sometimes they are helpful because I can treat them as directions not worth pursuing.

|

While I don’t have scientific evidence that definitively tells me whether AI is adding to our mental faculties, you can sense which way I have buttered my bread.

Asking the right questions

The question “Is AI making us dumb?” is not the right question. The real challenge that technology has changed the basis on which we expect thinking to occur, and we haven’t made our new expectations clear. It’s an exponential gap.

Few marathon runners would complete a race using a car. The point is the race.

Getting ChatGPT to do your thinking is a bit like finishing the marathon in a car. So let’s investigate the motivations for doing that. Perhaps people don’t value the thing they are doing and just want to get it done? Perhaps they can’t judge what excellent is, so they will be satisfied with good? Perhaps the activity is simply instrumental, a means to an end, not a constitutive activity with value in itself?

We’re asking people to think about college applications. Ostensibly, the application determines their suitability for the next four years. To get an AI to do it—rather than, perhaps, act as a Socratic critic—speaks to the perceived stakes of that application. The point is not that modern life will be full of AI; it is that to use AI well, you need to think well. Unless, of course, you’ve concluded that AI will always outthink you in all the ways that matter.

It’s also worth examining in the workplace. Of course, there are times when its appropraite to get a machine to do a task. I don’t grow my own cacao beans. But perhaps it reflects workplace environments geared to throughput rather than quality, agency and ownership?

To reverse Charlie Munger, show me the incentive, and I’ll show you the outcome. The outcome here is offloading important thinking to a chatbot. So what incentives produced it? We’ve developed tests, credentials and career ladders and cemented them across centuries of practice. They were built when cognition was scarce and scarcity paid well. Thinking proved you had that scarce asset, and we never needed to ask if you were actually the one doing the thinking. That isn’t true now, but the payoff for perfecting the scarcity theatre of a perfect GPA, Ivy education, and the rest remains.

So what system of incentives do we need that values (and motivates us) to use our actual brains?

And that, rather than whether AI is making us dumb, is the right question to ask.

And it is a much thornier one to answer.

Short morsels to appear smart at dinner parties

AI software engineering roles are growing and concentrating in the top-paying US companies according to the latest state of the software engineering job market by Gergely Orosz and Jessica Salmon.

Implementation expertise is in high demand.

And Anthropic is seen as the most desired company to work for, followed by starting one’s own business. via Lenny Rachitsky

Zilan Qian digs into China’s AI optimism: “perhaps every respondent genuinely believes that AI is good for both society and for themselves. Or perhaps they see AI as another surgery necessary to survival, knowing full well that flesh will be cut away and discarded.”

ByteDance is designing its own Groq-style AI accelerator chips to lessen its reliance on Nvidia.

Non-fiction book publishing is absolutely not ready for AI.

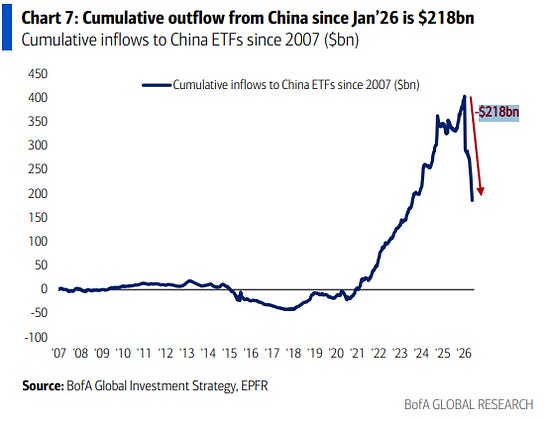

China ETFs are sinking.

|

Lack of sleep changes our gut microbiome.

How to weigh a cell. A nice piece by Niko McCarty

Anti-drone nets in Ukraine:

|

Thanks for reading!

Rerating is a fancy Wall St word that means “we’ve decided the thing we are looking at is now a different type of thing.”

I usually handwrite my essays and then read them aloud to Claude for transcription. Close-in edits happen on pen and paper on printouts. Final edits are back on the keyboard.

You're currently a free subscriber to Exponential View. For the full experience, upgrade your subscription.

![]()

![]()

Similar newsletters

There are other similar shared emails that you might be interested in: