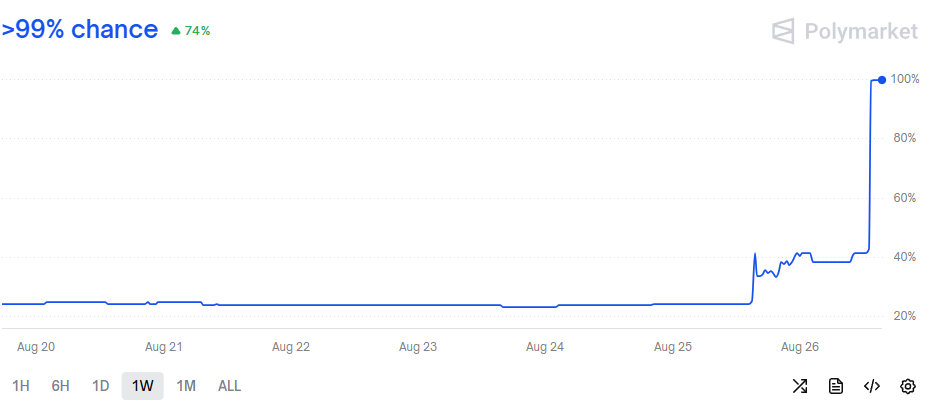

| Here’s the one-week chart of “Taylor Swift and Travis Kelce engaged in 2025?” on Polymarket, the prediction market: That spike yesterday afternoon — from about 43% to about 100% — came from Swift’s and Kelce’s official engagement announcement; the market has now resolved to “Yes.” The spike Monday afternoon — from about 25% to about 40% — did not come from the official announcement. Someone bought a lot of Yes contracts on Monday; Polymarket has an activity log, so you can see that user “romanticpaul” was a heavy buyer, starting at around 25 cents on Sunday; as of yesterday he was the top Yes holder, with 5,062 contracts. Each Yes contract pays out $1, so he made, you know, $3,500 or something on the trade. Romanticpaul had good timing. Did he have inside information, or did he just get lucky? I have no idea. Also he didn’t get that lucky; I suspect that $3,500 won’t buy the cheapest item on Swift’s and Kelce’s wedding registry. Still, it raised eyebrows. The internet tells me they actually got engaged two weeks ago. Surely somebody knew before yesterday. In the past, if you knew about Taylor Swift’s engagement before anyone else, you could have felt cool about it, or perhaps you could have sold the story to a tabloid. Now you can use prediction markets to turn it directly into, well, some money. You can be rewarded for making the market on Taylor Swift’s engagement more efficient. Three themes that we have talked about around here are: - Insider trading in the US stock market is illegal; there is lots of law about it and the rules are enforced pretty enthusiastically. But insider betting — using material nonpublic information to make sports bets — is more of a legal gray area, because legal sports gambling in the US is still fairly new. There is a decent argument that insider sports betting is a form of wire fraud (by analogy to insider trading being a form of securities fraud), and there have been some prosecutions, but there’s also a decent argument that it isn’t, and there haven’t been that many prosecutions. (Not legal advice.)

- For weird and accidental reasons, a new and appealing way to do sports gambling — really any gambling — in the US is through prediction markets that are regulated as commodity exchanges by the US Commodity Futures Trading Commission. Kalshi, a CFTC-regulated prediction market, now lists sports contracts, and those contracts seem to get better regulatory and tax treatment than ordinary sports bets would get. (Kalshi also lists Taylor Swift wedding contracts.) And Polymarket also now has a CFTC-registered derivatives exchange.

- Insider trading on prediction markets is also a bit of a gray area. Kalshi bans insider trading. Manifold Markets, a play-money, non-CFTC-registered prediction market, loves insider trading, because it makes predictions more accurate. Polymarket is a little grayer; here is a 2024 Decrypt article saying that “a person familiar with Polymarket’s operations who requested anonymity to speak candidly [1] told Decrypt that insider trading ‘is strictly prohibited’ by the company’s terms of service,” but noting that the terms of service don’t actually say that. What they say is that you can’t do anything that violates applicable law. Does insider trading on Polymarket violate applicable law? Maybe!

So, if you use inside information to bet on sports or weddings on a CFTC-registered futures exchange, is that … commodities fraud? The traditional answer is “insider trading is not about fairness, it’s about theft”: If you have inside information and some obligation to the owner of the information not to use it, then it’s illegal to trade on it. [2] (If you shot Swift’s and Kelce’s engagement photos and signed a nondisclosure agreement, you can’t trade.) If you have inside information and you are the owner of that information, whatever, go nuts. (If romanticpaul is Kelce, fine? Also very cool.) Most conceivable sports insider trading would probably be illegal: Sports leagues are normally quite strict about prohibiting their players and employees from betting, certainly on their own games, so a player betting based on inside information would surely be violating a duty of confidentiality. But this is all speculation and not legal advice. And there is a lot of non-sports betting — sorry, predicting — where the rules are even fuzzier. Bloomberg’s Francesca Maglione reports: Taylor Swift’s engagement to football star Travis Kelce has sparked a flood of online bets on the billionaire singer’s life. On prediction market websites like Kalshi and Polymarket, traders are putting money behind their expectations for the couple. … Gamblers on Kalshi can now make wagers on the wedding timeline, with about $80,000 worth of bets already placed in the hours after Swift's post, according to the company. On Polymarket, bettors are going so far as to gamble on when the couple might have a baby, while also growing more convinced that the singer will headline the 2026 Super Bowl halftime show. Anyway I look forward to the first CFTC insider trading enforcement action about sports betting. Or sports-adjacent proposition betting. Or wedding date betting. Everything is sports, and everything will be commodities fraud. I sometimes describe crypto treasury companies as “perpetual motion machines.” The idea is: - You issue 100 shares of stock for $1 per share, raising $100, and buy $100 worth of Bitcoin.

- Now you have a net asset value of $100 (the Bitcoin), but for some reason your stock trades at $2 per share, for a $200 market capitalization. The stock market will pay $2 for $1 worth of Bitcoin, and you benefit from that anomaly.

- You sell 100 more shares of stock for $2 per share, raising $200, and buy $200 more of Bitcoin.

- Now you have 200 shares outstanding, your net asset value is $300 ($1.50 per share), your market cap is $600, and your stock is worth $3 per share.

- You keep doing this forever, buying more Bitcoin and increasing your stock price.

Obviously I am kidding a little. There is no such thing as a perpetual motion machine. This has to end. But how? Well, my point in laying it out like this is mostly that you can’t sell stock at 200% of net asset value forever: Eventually people will stop paying a premium to buy your stock, and then the trade doesn’t work anymore. You can’t sell infinite shares to buy infinite Bitcoins, because eventually you will run out of people to sell stock to. And there are some signs that the generic “the stock market will pay $2 for $1 of crypto” trade has stopped working as well as it used to. MicroStrategy Inc., which invented this idea, still trades at a premium to its Bitcoin value, but that premium is no longer 100%, and some other crypto treasury announcements have fizzled. But there’s another reason this trade can’t go on forever, which is that there will only ever be 21 million Bitcoins in the world. You can’t issue infinite shares to buy infinite Bitcoins, because there are not infinite Bitcoins. I am a skeptic of this trade, so I assume that you’ll run out of buyers for your shares long before you run out of Bitcoins to buy, but if you are very bullish on crypto treasury companies you might take the opposite view. One theoretically conceivable endgame for MicroStrategy would be: - Right now, the total supply of Bitcoin is worth about $2.2 trillion; MicroStrategy owns about $70 billion worth (about 3% of the total supply) and has a market capitalization of about $100 billion.

- It keeps issuing more shares to raise more money to buy more Bitcoins.

- It buys so much that it pushes up the price of Bitcoin, but the price of its stock goes up to match, so it can keep raising more money to buy more Bitcoins.

- Eventually the total supply of Bitcoin is worth, say, $10 trillion, MicroStrategy owns $9.99999 trillion worth — all of the Bitcoins but one — and its stock trades at $13 trillion.

- Then MicroStrategy goes and buys the last Bitcoin in circulation: Now it owns 100% of the Bitcoin in the world, and the only way to get Bitcoin exposure is to buy MicroStrategy stock.

- ???

I don’t know if that would be desirable, or why, or what would happen next. Nor do I think that this is practically possible, for reasons like “not everyone would sell their Bitcoins to MicroStrategy” [3] and “there are a bunch of other Bitcoin treasury companies these days” and “come on people are not going to buy MicroStrategy stock at a $13 trillion valuation, this is all stupid.” But I guess it is all theoretically possible. If a crypto treasury company really is a perpetual-motion-ish flywheel, then the natural endpoint is for the treasury company to own all of the crypto. If the crypto is worth twice as much in a treasury company as it is outside of the treasury company, it will migrate to it most valuable use. Again: stupid! But here is a Trump Media & Technology Group Corp., uh, thing: Trump Media & Technology Group Corp. and Crypto.com agreed to a deal with blank-check vehicle Yorkville Acquisition Corp. to create a crypto treasury company focused on buying and holding CRO tokens, the native cryptocurrency of the Cronos ecosystem. … Shares of Trump Media rose as much as 10.2% on Tuesday, while Yorkville Acquisition stock fell as much as 3.4% in New York. Cronos token prices gained 32.3% on Tuesday, according to tracker CoinMarketCap. ... Cronos has a total market value of about $6.5 billion, making it the 23rd largest cryptocurrency, according to CoinMarketCap. It is the native token of the Cronos blockchain, which is supported by Crypto.com. … Funding for the SPAC, which will be called Trump Media Group CRO Strategy Inc., is expected to consist of 6.3 billion CRO tokens representing about 19% of the total CRO outstanding, as well as $200 million in cash, $220 million in mandatory exercise warrants and a $5 billion equity line of credit with an affiliate of Yorkville Acquisition Sponsor, the backer of the Yorkville Acquisition special purpose acquisition company, the filing shows. Details of the expected funding were not disclosed. The fact that the special purpose acquisition company’s stock fell (it trades at roughly its cash value) suggests that in fact you can’t sell Cronos tokens on the stock exchange for much of a premium, but whatever. The point here is that the crypto treasury company is planning to raise something like $6.6 billion [4] to buy tokens with a total market cap of $6.5 billion. Perhaps its buying will push up the market cap, but we are talking roughly 100% coverage. Weird? The press release leans into this, saying that the company will have “what we believe to be the largest digital asset treasury company to market cap ratio in history,” definitely a ratio that will be in the next edition of all the finance textbooks. Also: “The sheer size and structure of this project will encompass more than the entire current market capitalization of CRO, with the additional commitments of over $400 million in cash and a further $5 billion line of credit facility to acquire additional CRO,” said Kris Marszalek, Co-Founder and CEO of Crypto.com. “This, combined with share lock-ups by each party and the treasury’s validator strategy, make it a unique and compelling offering compared to all other digital asset treasuries.”

Is the plan to … buy all the tokens? No? “The Cronos ecosystem is already thriving with DeFi protocols, multi-asset marketplaces and more, anchored by the CRO token as both a utility and governance asset,” says the press release, and the CRO token doesn’t have much utility if you put 100% of it in a treasury company. Still I suppose if you put almost all of the tokens in a treasury company, that would support its price, possibly more than utility would. If the most valuable use of crypto tokens is stashing them in publicly traded treasury companies, eventually that’s where they will all end up. At some level of abstraction, the way a big hedge fund works is that it hires some researchers, it asks them to find ways to predict stock prices, and then it trades stocks based on their predictions. If they work, the hedge fund makes money, and the researchers get a cut of the money. If they don’t work, the hedge fund loses money, and the researchers get fired. This is a generic description, and it covers both fundamental analysts (who cover a smallish universe of companies, understand them deeply, and make high-conviction bets on the particular companies they think will outperform) and quantitative researchers (who cover all the stocks, look for statistical relationships and make thousands of low-conviction probabilistic bets on which sorts of stocks tend to outperform). So the key skills of the researchers will vary; they could be financial analysis or machine learning or whatever. But the key skills for the fund are [5] : - Hiring good researchers;

- Checking their predictions to make sure they are good before trading on them;

- Managing risk to make sure that, when a prediction stops working, the fund stops trading on it; and

- Firing researchers whose trades don’t work.

And those are the essential attributes of the big hedge funds: They’re good at hiring (“We are a massive filter of talent,” Gappy Paleologo said on the Money Stuff podcast), they’re good at allocating capital and managing risk, and they’re quick to fire portfolio managers who have big drawdowns. A successful multi-manager hedge fund is an analytical, medium-term investor in investors. The normal way to do this is with a hiring process and a human resources department [6] and a risk management department. Basically a fundamental approach. But you could imagine a quantitative, probabilistic approach, too. Here’s a Bloomberg News story about Numerai: A crowdsourcing hedge fund backed by the billionaire Paul Tudor Jones looks poised to more than double in size with a big influx of cash from JPMorgan Asset Management. San Francisco-based Numerai LLC says it has secured a commitment of as much as $500 million from JPMorgan Chase & Co.’s asset-management arm to be deployed over the next year. The quantitative firm currently runs about $450 million. Numerai, which launched its first fund in 2019, buys and sells stocks based on trading ideas sourced from freelance finance quants. The latter are compensated in the firm’s native cryptocurrency, which they also use to signal confidence in their forecasts. … Numerai itself lost 17% in 2023. [Richard Craib, Numerai’s founder] said his team then tweaked the fund’s playbook so that it ditched losing trades more quickly. A smaller pool of high-quality users contributed to the subsequent recovery. The normal approach at a big hedge fund is to interview a smallish universe of potential portfolio managers, understand them deeply, and make high-conviction bets on which of them will outperform. (And then fire them quickly if they don’t work out.) The Numerai approach is to hire everyone, look for statistical signals of predictive ability, make more but lower-conviction bets on them, and then, of course, fire them quickly if they don’t work out. OpenAI Employee Stock Sale Could Rise to $8 billion. Microsoft talks set to push OpenAI’s restructure into next year. Hedge Funds Are Shorting the VIX at a Rate Not Seen Since 2022. Convertible arbitrage is doing well. Trump’s Fed Gamble Risks Pushing Key Bond Rates Even Higher. Alex Gerko earned £682mn from trading firm XTX in 2024. Spy Satellites, Road Cameras, Phone Trackers: How Alternative Data Companies Are Changing Investing. Venture Debt Firms Tilt Toward Mature Companies. An 83-Year-Old Pizza Tycoon Fights to Save 3,500 Domino’s. Young European Backpackers Are Being Lured to Australia for Mining Jobs. Lamborghini CEO says tariffs are causing even the wealthiest buyers to pause. Cracker Barrel Scraps New Logo After Backlash. Prosecutors Fail to Secure Indictment Against Man Who Threw Sandwich at Federal Agent. If you'd like to get Money Stuff in handy email form, right in your inbox, please subscribe at this link. Or you can subscribe to Money Stuff and other great Bloomberg newsletters here. Thanks! |